I’ve just come back from a week in Brussels, a city that gets so much right, but especially public transport. I enjoyed my time there very much, but along with the green spaces and good food, the thing that stood out to me most was how easy it was to get around. As a tourist, nothing could be easier than using the trams and buses. There are signs EVERYWHERE showing the routes, and the trams even have electronic boards with little lit-up dots showing you where all the trams on the line are currently at. Finally - and most crucially for this blog post - payment was entirely frictionless. As dozens of advertising boards say across the city, “Your bank card is your ticket”, meaning that contactless is supported everywhere.

To pay for the tram, I could simply tap my debit card on the reader continuously throughout the day, and then once the day was finished, I would get charged the daily cap, or the sum of my individual journeys, whichever would be the better value. User-friendly to the extreme! It made one of the more stressful aspects of holidays, transport, so much easier, and for that I thank Brussels and I thank Belgium.

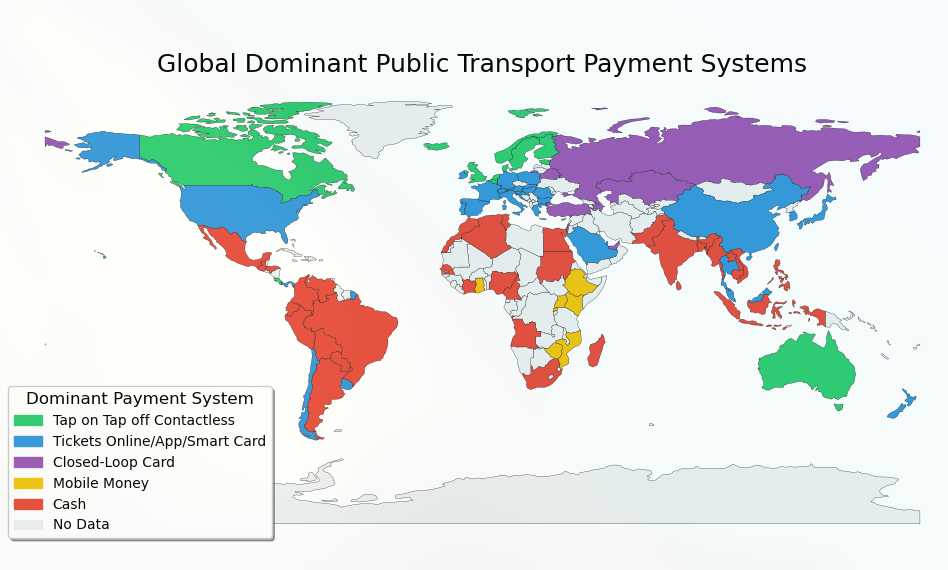

Brussels isn’t the only one getting this right. London remains the global gold standard for this, having rolled out contactless on buses way back in 2012 and across the tube by 2014. Nowadays, contactless journeys completely dwarf the old Oyster card usage - around 1.6 billion trips a year compared to a fraction of that on Oyster, saving TfL a fortune in fare collection costs. This model is gradually rolling out across the UK’s fragmented rail network too, joined by cities like Manchester, Edinburgh, and Nottingham.

Other countries are catching up, or even overtaking. The Netherlands achieved the dream in 2023 with “OVpay”, the world’s first nationwide open-loop system. One tap works for every train, tram, and bus in the entire country, with no regional boundaries or separate tickets required. Singapore’s “SimplyGo” is similarly comprehensive, using transit as a way to get people comfortable with using mobile wallets for everything. Even Canada, which stuck with proprietary cards like Presto for a long time, is seeing a rapid shift - Ottawa’s system now caps spending automatically on bank cards, just like London.

This seamless experience just makes the hassle you encounter elsewhere all the more frustrating. Paris, for example, is currently in a messy transition. It used to use ‘carnets’ (packs of 10 paper tickets), and if you don’t use them all, sucks to be you. Recently, those were decommissioned at several stations but instead of allowing contactless, you now have to either buy a physical Pass Navigo (come on, Parisiens) or download the buggiest app known to man, IDF Mobilité, and pray your phone’s NFC works this time. While they are finally phasing out magnetic strips, they’re still playing catch-up compared to their neighbours.

Strasbourg is similar; while it is a beautiful city with trams I absolutely adore, I would have adored them a lot more if I could ‘tap on tap off’. Instead, I was stuck calculating the best combination of tickets to buy for the group, finally settling on some ‘24HR Trio’ tickets, and then having to keep track of the time we first validated them. Validation is another pain point common across Europe. It makes sense in theory, but having to validate a ticket every time you use it is an absolute pain. It’s easy enough to do, but I’ve heard horror stories of people forgetting and being fined hundreds of euros, despite having genuinely bought the ticket, just because they forgot to tap it on some obscure metal pole in the corner of the station.

These might all sound like gripes and whines of an entitled tourist, but I think it’s an important aspect which affects how it feels to live and work in a city. Anything that reduces friction to public transport is a good thing as it reduces our reliance on cars. However, the “tap a bank card” model isn’t the only solution. In China, the system is entirely built around QR codes within “Super Apps” like Alipay and WeChat Pay, which 90% of people use for daily purchases. Germany’s “Deutschlandticket” offers unlimited regional transport for €49 a month, shifting focus entirely to a digital subscription model. Japan and South Korea have “virtualized” their existing proprietary cards (Suica, Pasmo, T-money) into mobile wallets, keeping the speed of their specific NFC tech while adding the convenience of phone top-ups.

Meanwhile, places like the US remain a patchwork of regional apps and systems, although NYC’s OMNY is excellent. Developing markets like India, Brazil, and Indonesia are often leapfrogging cards entirely, moving straight from cash to mobile money and real-time payment systems like UPI and Pix. Ultimately, whether it’s a card, a phone, or a QR code, the shift is clearly towards making the payment part invisible. The less we have to think about how to pay for a journey, the more likely we are to take it.

A map of countries by dominant transit payment system:

Sources: Visa Future of Urban Mobility, Mastercard Mobility Whitepaper, UITP Economic Outlook 2024, and various transit authority reports.